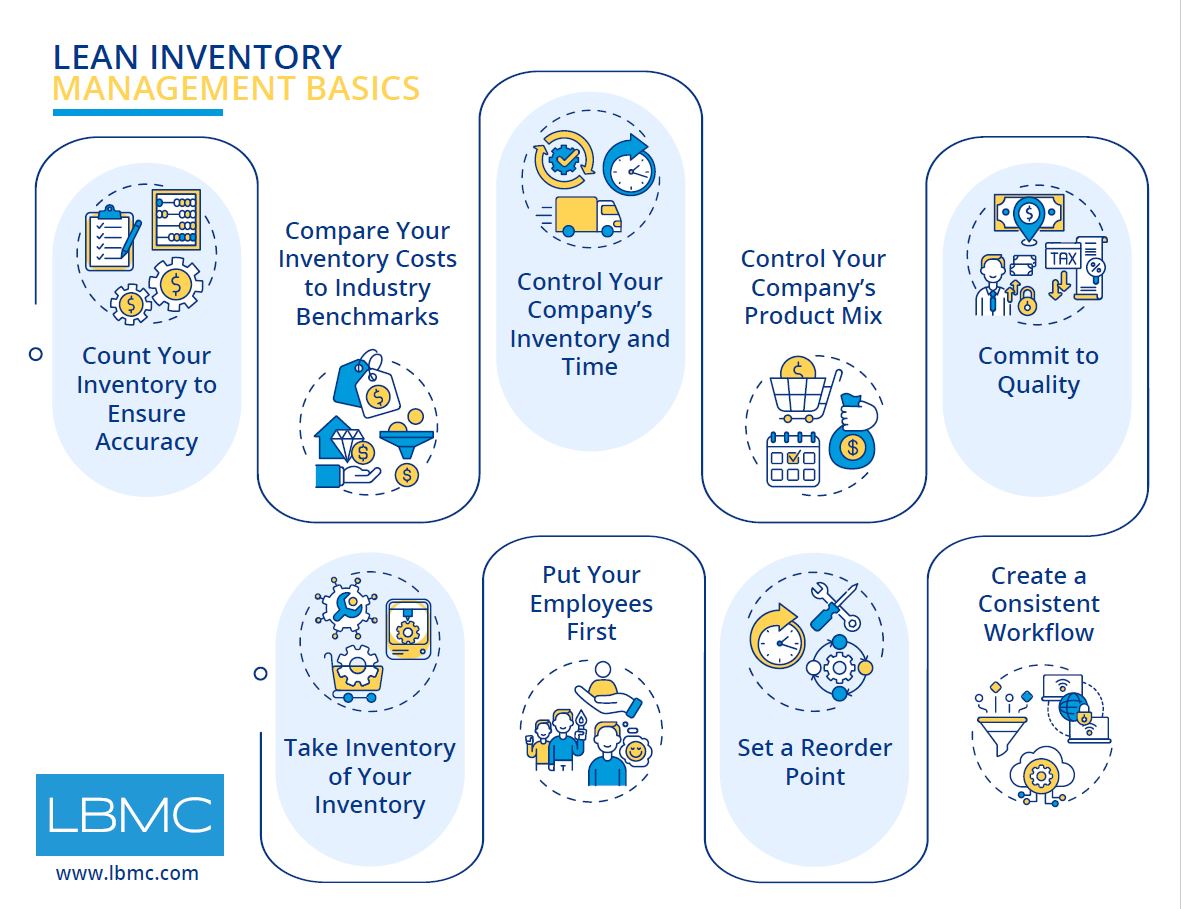

After you have counted and corrected your inventory records, you should compare your inventory costs to those of other companies in your industry. Trade associations often publish benchmarks for:

- Gross margin [(revenue – cost of sales) / revenue],

- Net profit margin (net income/revenue), and

- Days in inventory (average inventory / cost of sales) x 365

Your company’s goals should be to at least meet industry standards. For a retailer, inventory is simply purchased from the manufacturer, but the inventory account is more complicated for manufacturers. Inventory costs for manufacturing companies consist of raw materials, labor and overhead costs. It’s commonplace for manufacturing and distribution companies to use standard cost to value their inventories.

The composition of your company’s cost of goods will guide you on where to cut. In a tight labor market, it’s hard to reduce labor costs. However, it may be possible to renegotiate prices with suppliers. Your company should also be sure to monitor commodity fluctuations, such as steel or aluminum for example, in anticipation of future increases to material costs. It may be possible to renegotiate sales prices with customers based on these anticipated changes.

The carrying costs of inventory, such as storage or insurance, can also be negotiated to improve margins. Other carrying costs, such as obsolescence and pilferage, can decrease with internal improvements. For example, your company could negotiate a new lease for your warehouse, install anti-theft devices, or opt for less expensive insurance coverage, if appropriate.